.svg)

Understanding Equivalent Yield in Commercial Property Valuations

%20(2).png)

Equivalent yield is one of the most widely used valuation metrics in commercial real estate across the UK and Ireland.

Despite being a foundational concept for valuers, agents, and investors, it is still often misunderstood outside the profession.

This article explains what equivalent yield means, why it matters, how it is calculated in practice, and how Pantera brings a new level of clarity and transparency to the calculation.

What is Equivalent Yield?

Equivalent yield represents the single discount rate that, when applied to a property’s future income stream, produces its current capital value.

In simpler terms, it blends today’s passing income with tomorrow’s market-level income (ERV), and expresses the relationship as a long-term return.

How Equivalent Yield Compares to Other Yield Measures

Analysts often consider three complementary yields:

Net Initial Yield

Based on current passing rent — a snapshot of return today.

Reversionary Yield

Based on market rental value once leases roll to ERV.

Equivalent Yield

Equivalent yield typically sits between the net initial yield and reversionary yield, reflecting the transition from secure income at passing rent to fully reversionary income.

This makes it a balanced measure that accounts for both current performance and future potential.

Why Is Equivalent Yield Useful?

It provides:

- A single comparable income-based return metric

- Visibility of whether income is improving or eroding over time

- A consistent benchmark across sectors, locations, and asset types

- A way to quantify the impact of lease expiry risk

Unlike IRR-style cashflow models, equivalent yield remains especially prevalent in the UK and Ireland, where the valuation community favours a blend of assured and reversionary income to arrive at capital value.

Nominal vs True Equivalent Yield

There are two versions of equivalent yield, both based on the same underlying rent stream but with different payment timing assumptions.

Nominal Equivalent Yield

Assumes rent is paid in arrears, at the end of a period.

It is the version most commonly quoted because:

- Historic comparable evidence is collected on this basis

- Agency and valuation templates standardise around arrears assumptions

- It is embedded into most professional training, manuals, and lender methods

True Equivalent Yield

Assumes rent is paid in advance, meaning income arrives earlier.

Because of this timing shift:

- Present value of the rent stream increases

- The discount rate required to match capital value is slightly lower

- The variation can become meaningful on short income or heavy turnover portfolios

Understanding which basis is being used is essential when comparing yields between assets.

Why Equivalent Yield is Hard to Calculate in Practice

Textbook examples typically show a single-tenant building, with a rent stream, a void, and a re-letting back at ERV.

But real buildings are rarely that simple.

In a multi-let asset, each unit may have:

- A different passing rent

- Unique expiry dates

- Rent free periods

- Different incentive levels

- A void before re-let

- ERV uplift or drop

- Potential over-renting or under-renting

- Breaks and sequencing risks

Blending all of that into a single discount rate manually is slow, error-prone, and extremely difficult to audit — which is why valuers lean on software.

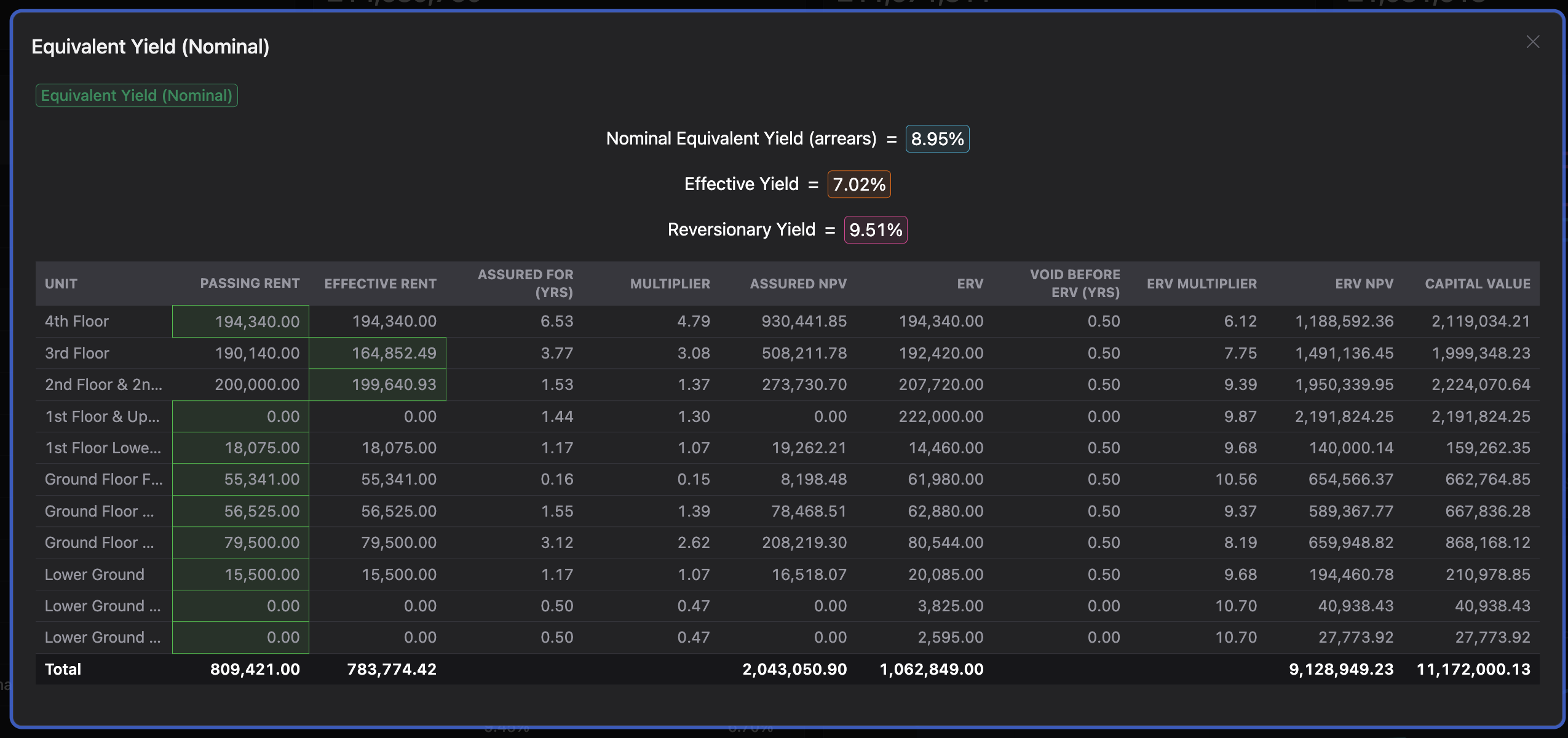

Example: Unit-by-Unit Breakdown

Pantera shows the full calculation rather than just the final result.

In the example building below, each unit contributes differently based on its rent, expiry, void, and ERV position.

You can see:

- Passing rent

- Effective or headline rent

- Lease term remaining

- Assumed void period

- ERV achieved thereafter

- NPV of assured vs reversionary income

- Capital value contribution per unit

This transparency is extremely useful for valuation justification and client reporting.

Over-Rented Units and Reversionary Impact

Some units in the screenshot are over-rented, meaning the passing rent is above ERV.

When these leases expire:

- Income drops to ERV

- Reversionary NPV falls

- Capital value contribution declines

Equivalent yield expresses this numerically — helping analysts quantify how much income risk is embedded in the current rent roll.

Effective Rent and Rent Free Adjustments

Two of the units show an effective rent rather than the headline passing rent.

This reflects the structure of the leases: built-in rent free periods that apply when break clauses are ignored.

Pantera automatically:

- Calculates the blended rent

- Applies the correct timing

- Shows the breakdown when hovering

This means the model doesn’t hide free rent or incentive effects — it explains them.

Extending the Void: Rent Free Assumptions on Re-Let

Another modelling nuance is the treatment of incentives on new lettings.

Many valuers assume:

- The tenant will leave at expiry

- A void will occur

- ERV is not achieved immediately

- A rent free period applies before full rent resumes

These assumptions shift cashflows further into the future, reducing:

- Present value

- ERV NPV

- The resulting equivalent yield

Software makes these iterative assumptions manageable, repeatable, and visible.

Why Pantera Helps Valuers Work With Confidence

Equivalent yield remains a powerful and widely used metric — but it is also highly sensitive to timing, lease structure, and income profile assumptions.

Where many valuation tools output only the final number, Pantera goes further:

- It exposes the drivers behind each unit

- It shows assured vs reversionary NPV

- It makes rent-free, void, and break logic transparent

- It gives valuers a calculation they can defend, explain, and teach

For teams training graduates, onboarding new hires, or defending valuation conclusions to investment committees or lenders, this level of visibility matters.

Pantera does not replace professional judgement — it supports it by showing exactly where the numbers come from.

Final Thought

Equivalent yield sits at the heart of commercial property valuation across the UK and Ireland.

Whether assessing a simple lease or a ten-unit office, the logic is the same: today’s rent versus tomorrow’s market reality.

Understanding why the equivalent yield is what it is can be just as valuable as the figure itself.

Pantera makes that understanding clearer, faster, and easier to communicate — from analyst to partner to client.

Related blogs

Customer Story: Pantera Has Changed the Way We Work

Avison Young's capital markets team went from an hour just to set up a model, to a client-ready appraisal in under ten minutes. Sam Hume-Kendall explains how.

Why Vertical AI wins in Real Estate

Why generic AI tools will not be good enough for the firms that underwrite, lease, and invest in property, and what embedded, vertical AI does instead.

IRR vs Equity Multiple: When Each One Matters

IRR and equity multiple both measure return. But they measure different things and optimising for one can mean ignoring what the other is telling you.

Future-proof your

property business