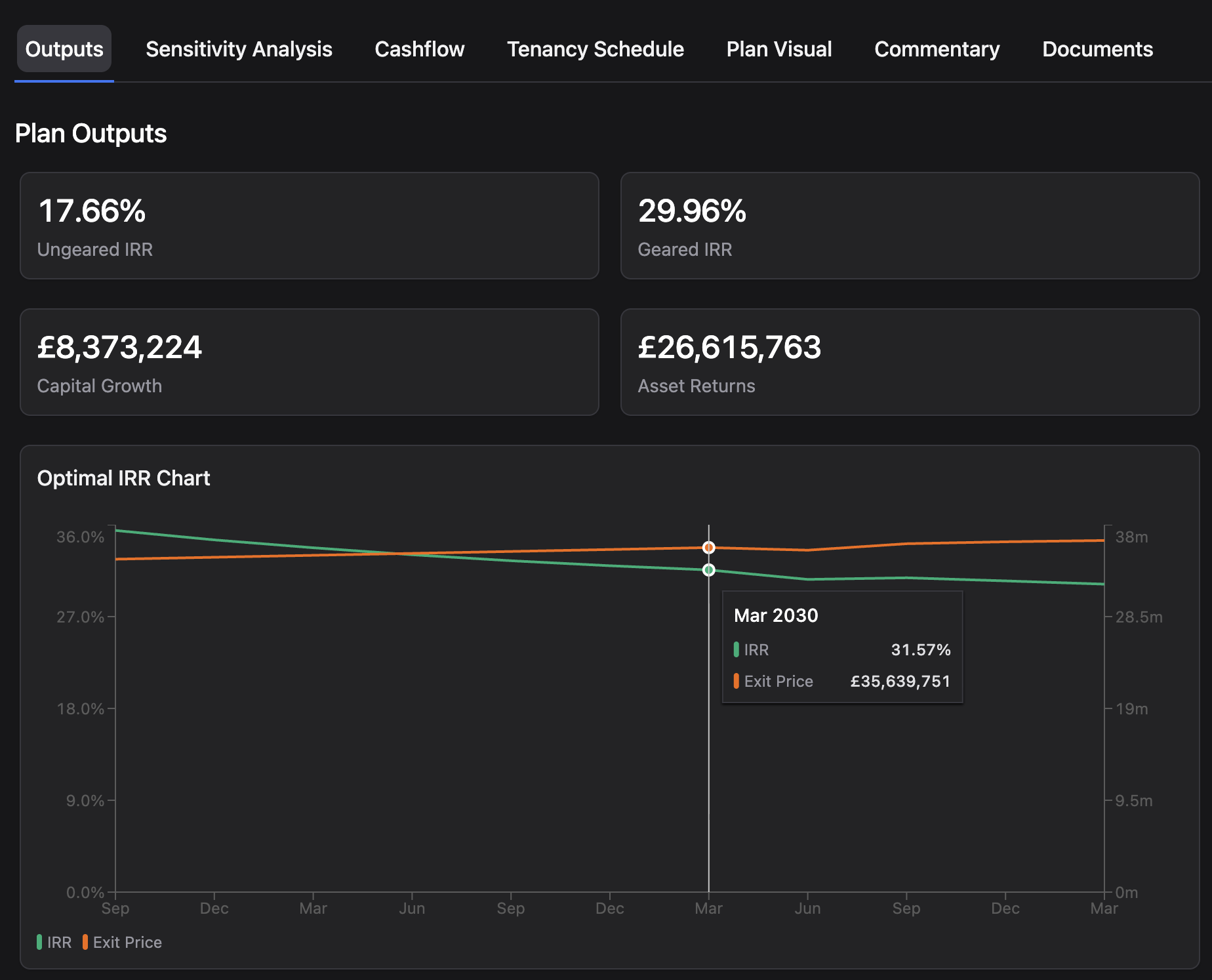

.svg)

Geared vs Ungeared IRR: What the Difference Reveals About a Deal

The same deal, two different returns

When someone quotes the IRR on a real estate deal, the first question worth asking is: geared or ungeared?

Both measure the annualised return generated by a set of cashflows over time. But they measure it from a different starting point - and that distinction changes the number significantly, and changes what the number is useful for.

Ungeared IRR looks at the return from the asset itself, ignoring how it was financed. geared IRR looks at the return to the equity investor, after accounting for the cost and timing of debt.

Neither is more correct. They answer different questions.

Ungeared IRR: the asset return

Ungeared IRR treats the property as if it were purchased entirely with equity. There is no debt in the model. The cashflows are simply the income generated by the asset and the proceeds from eventual sale, discounted to produce a single annualised return figure.

This is useful because it isolates the quality of the underlying investment. Two deals with identical ungeared IRRs are generating the same return from the asset regardless of how they are structured. It strips out the impact of financing and lets you compare like with like.

It is also the metric lenders tend to focus on, because it reflects the asset's ability to service and repay debt without depending on the investor's financing structure.

Geared IRR: the equity return

Geared IRR runs the same calculation but only on the equity cashflows. The purchase price is reduced by the loan amount, debt service is deducted from income, and the loan is repaid at exit. What remains is the cashflow to equity, and the IRR on that cashflow is the geared return.

Because equity is a smaller number than the total asset value, the same absolute profit produces a higher percentage return. Debt amplifies the equity return - in both directions.

This is the number that matters most to equity investors. It reflects what they actually receive relative to what they put in.

What the gap between them reveals

The spread between geared and ungeared IRR is where the real insight sits.

If the ungeared IRR is 8% and the geared IRR is 14%, debt is doing meaningful work. The financing structure is amplifying returns significantly. That might be appropriate, but it also means the deal is more sensitive to things going wrong - voids, cost overruns, interest rate movement.

If the spread is narrow - say 8% ungeared and 9% geared - debt is barely moving the needle. That might mean the LTV is low, or the cost of debt is close to the asset return, or the loan terms are conservative. Not necessarily a problem, but worth understanding.

If leverage is actually reducing the equity return relative to the ungeared figure, the cost of debt is higher than the asset is generating. The deal is negatively geared. Capital is being destroyed at the financing level even if the asset is performing.

Why both numbers matter in underwriting

A strong geared IRR on its own is not enough to underwrite a deal. If it is being driven primarily by aggressive leverage rather than asset performance, the risk profile is different to a deal generating the same equity return from a lower LTV position.

Equally, a conservative ungeared IRR does not automatically mean a weak equity return. With the right financing structure, a steady income-producing asset can deliver attractive geared returns without taking on significant asset risk.

Using both figures together gives investment committees and lenders a more complete picture: how good is the asset, and how much is the financing doing to get us to that return?

The role of debt cost and duration

Two variables have the biggest impact on the spread between geared and ungeared IRR: the cost of debt relative to the asset yield, and the loan term relative to the hold period.

If debt costs less than the asset yields, leverage is positive - every pound of debt deployed adds to the equity return. If debt costs more, leverage destroys value at the margin.

Duration matters because interest compounds over time. A short-term loan on a long hold period may have a very different effect on geared IRR than a loan matched to the exit. Modelling the actual cashflow timing - drawdowns, interest, repayment - is the only way to see this clearly.

How Pantera models both

Pantera calculates both ungeared and geared IRR as standard outputs within the same model. Debt assumptions - LTV, interest rate, drawdown schedule, and repayment timing - are built directly into the cashflow rather than applied as a blunt adjustment. This means the geared return reflects how the deal actually works, not a simplified approximation.

Seeing both figures side by side, with the full cashflow detail behind them, makes it straightforward to understand what the financing is doing to the return - and to test what happens when debt terms change.

Final thought

Geared and Ungeared IRR are not competing metrics. They are complementary lenses on the same deal. The ungeared figure tells you about the asset. The geared figure tells you about the equity position. The gap between them tells you about the risk embedded in the financing structure.

Reporting one without the other leaves part of the story untold.

Related blogs

Why Vertical AI wins in Real Estate

Why generic AI tools will not be good enough for the firms that underwrite, lease, and invest in property, and what embedded, vertical AI does instead.

IRR vs Equity Multiple: When Each One Matters

IRR and equity multiple both measure return. But they measure different things and optimising for one can mean ignoring what the other is telling you.

%20(2).png)

Understanding Equivalent Yield in Commercial Property Valuations

Equivalent yield is a core UK valuation metric that blends current and future income. This article explains how it works and how Pantera makes the calculation transparent and defensible.

Future-proof your

property business