.svg)

IRR vs Equity Multiple: When Each One Matters

Two numbers, two questions

IRR and equity multiple are the two most commonly used return metrics in real estate investment. Most deal summaries show both. Most investment committees ask about both. But they are not interchangeable, and the situations where one is more useful than the other are worth understanding.

IRR (internal rate of return) is a time-weighted measure. It tells you the annualised return on invested capital, accounting for when cashflows occur. A pound returned in year one is worth more to IRR than a pound returned in year five.

Equity multiple is simpler. It tells you how many times you get your money back. If you put in £10m and receive £18m in total, your equity multiple is 1.8x. Time does not factor into it at all.

Why IRR rewards speed

Because IRR is time-sensitive, it favours deals that return capital quickly. A development that delivers profit in 24 months will show a higher IRR than one delivering the same absolute profit over 60 months, even if total money made is identical.

This makes IRR a good metric for comparing deals where the hold period is similar. It captures the opportunity cost of having capital tied up. The faster you get it back, the sooner it can be redeployed.

But it creates a blind spot. A deal with a high IRR might not be generating much absolute return. A short hold with a small profit can show an impressive annualised figure that looks better than a longer deal which actually made significantly more money.

Why equity multiple captures what IRR misses

Equity multiple answers the most basic investor question: how much did I actually make?

A 1.4x equity multiple means you got 40% of your invested capital back as profit. A 2.5x means you more than doubled your money. These are intuitive, comparable, and unaffected by the timing of cashflows.

For long-hold strategies like core or core-plus funds, for example, equity multiple often matters more than IRR. An investor committing capital for ten years cares primarily about how much wealth has been created over that period. Whether the IRR was 9% or 11% is secondary if the multiple is strong.

Where the tension shows up

The clearest illustration is when comparing deals with different durations.

Deal A has a higher IRR. Deal B creates significantly more wealth. Which is better depends entirely on what the investor is trying to achieve and what they would do with capital if returned after year three.

If capital can be reliably redeployed at 12% or above, Deal A is the right choice. If the reinvestment opportunity is uncertain, Deal B may be preferable. Locking in a strong multiple without depending on future deployment.

The reinvestment assumption problem

IRR contains an implicit assumption that often goes unexamined: that all interim cashflows are reinvested at the same rate as the IRR itself.

In practice this rarely happens. If a deal generates an 18% IRR partly because of aggressive early distributions, those distributions need to find a home at 18% to justify the figure on a like-for-like basis. For most investors, that reinvestment rate is optimistic.

Equity multiple has no such assumption. The money either comes back or it does not.

What each metric is used for in practice

- IRR is the primary metric for value-add and opportunistic strategies, where timing of exit and active management drive the return

- Equity multiple is the primary metric for core strategies and longer hold periods, where wealth creation over time is the objective

- Development appraisals typically show both. IRR captures the time cost of the build period, equity multiple captures total return

- Lenders focus on neither directly, but understanding equity metrics helps explain sponsor motivation and alignment

Using them together

The most useful approach is to read IRR and equity multiple as a pair. A high IRR with a low multiple suggests a short deal with modest absolute returns. A high multiple with a modest IRR suggests a long hold that created real wealth but had capital tied up for an extended period.

A deal that scores well on both is a genuinely good outcome. The two metrics converging at attractive levels is a better signal than either one in isolation.

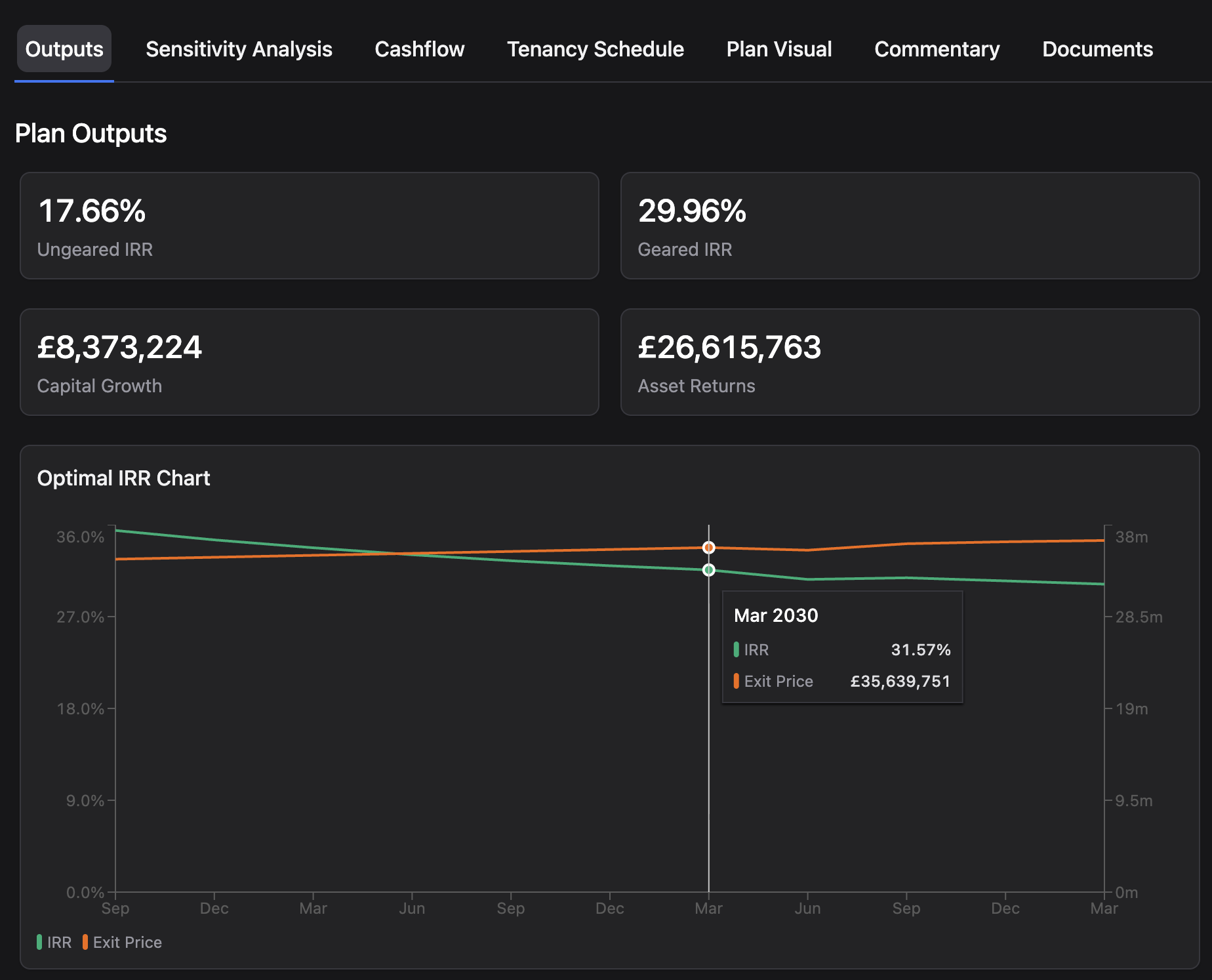

How Pantera presents both

Pantera outputs IRR and equity multiple together as standard return metrics, alongside the full cashflow that drives them. Running scenarios across different hold periods shows directly how IRR and equity multiple trade off against each other, supporting better investment decisions rather than optimising for a single headline number.

Final thought

IRR tells you how efficiently capital is being used. Equity multiple tells you how much wealth is being created. A complete picture of any deal requires both.

Reporting one and ignoring the other is a good way to tell half the story.

Related blogs

Customer Story: Pantera Has Changed the Way We Work

Avison Young's capital markets team went from an hour just to set up a model, to a client-ready appraisal in under ten minutes. Sam Hume-Kendall explains how.

Why Vertical AI wins in Real Estate

Why generic AI tools will not be good enough for the firms that underwrite, lease, and invest in property, and what embedded, vertical AI does instead.

Geared vs Ungeared IRR: What the Difference Reveals About a Deal

When someone quotes the IRR on a real estate deal, the first question worth asking is: geared or ungeared? This article explains what each measure actually captures, why the spread between them matters, and what it tells you about the role debt is playing in a deal.

Future-proof your

property business